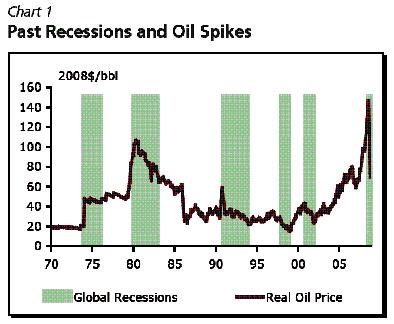

According to Deutsche Bank, there is a 60% chance that United States will enter recession during the next 12 months. This possibility is the highest since the last financial crisis.

The mathematical and economic model developed by the German Bank has been able to predict all the last recessions. They occur when the different treasury yield curves (3 mo, 1 YR, 2 YR, 5 YR, 10 YR and 30 YR) begin to converge towards the same profitability value.

When the spread between bond values is 0, recession is imminent. The following graph shows the spread between the 10 YR - 2 YR yields. Shadow areas indicate recession. In some cases, the curve becomes inverted (there is less confidence in the future due to the imminent recession).

As we can observe, the spread between these two yields was only 0.91 at the beginning of this June, down from more than 2.6 points two years ago. Right now, the spread is just 0.85 points.

This trend is also manifesting itself when we look at the current spread between the whole set of treasury yields and the flattening yield curve.

According to the Deutsche Bank, if the 10 YR yield (right now at 1.45%) falls to 1.00%, recession will become almost unavoidable.

---------------------------------

Since the UK referendum the US yield curve has flattened to new post-crisis lows. The 3m10y spread is now 115 bps compared to 210 bps at the start of the year, and the 2y10y spread is just 85 bps versus 120 bps on January 1.

This relentless flattening of the curve is worrisome. Given the historical tendency of a very flat or inverted yield curve to precede a US recession, the odds of the next economic downturn are rising.

In our probit model, the probability of a recession within the next 12 months has jumped to 60 percent, the highest it’s been since August 2008. The model adjusts the 3m10y spread by the historically low level of short rates and it suggests that on an adjusted basis the curve has already appeared to be inverted for some time.

The yield curve had successfully signaled the last two recessions when the model output rose above 70 percent. If 10y yields rally to 1.00 percent and the 3m rate is unchanged, the implied recession probability from our model will reach that number. At current market levels, the market is just 40 bps from that distinct possibility.

This link is from 2 weeks ago:

https://mishtalk.com/2016/06/14/us-rece ... ank-model/

Whereas this one is from today:

http://www.zerohedge.com/news/2016-07-0 ... calculates