From: http://www.bloomberg.com/news/2013-04-1 ... wdown.html

Interesting that for years some economics “experts” had predicted China’s collapse would be due to a much too high a growth rate and thus folks should be cautious investing there. And now that growth has plummeted to about 5X that of the US more “experts” are warning about the dangers. But I would imagine the new numbers could represent real concerns for manufacturers in other countries. If the current growth is the equivalent of Goldilocks’s “just right” condition it could lock China into a sustained long term growth pattern. Can’t last forever, of course. But as I said the other day: it doesn’t matter how fast the bear can run but how fast the other guy can run. The new China numbers imply to this economics non-expert that they’ll be leading the pack for a long time regardless of how much we’re all slowing down.

One interesting tidbit regarding sustainability: “China doesn’t need to expand faster than 8 percent in part because the number of new workers from 15 to 24 years old, the main source of job seekers, has been in decline since 2010, according to Li Wei, a Shanghai-based economist at Standard Chartered Plc.”

PeakOil is You

CHINA STUCK WITH SUB-8% GROWTH

CHINA STUCK WITH SUB-8% GROWTH

![]() by ROCKMAN » Mon 15 Apr 2013, 13:18:10

by ROCKMAN » Mon 15 Apr 2013, 13:18:10

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by Plantagenet » Mon 15 Apr 2013, 13:43:08

by Plantagenet » Mon 15 Apr 2013, 13:43:08

AT first glance it seems bizarre that people are concerned that China's growth has slowed to only a bit under 8%----isn't that still great?

But

(1) you can't trust the Chinese data----if the government is reporting growth has to slowed to under 8% it might well be quite a bit worse.

(2) the "trend is not your friend here"---growth in China is definitely slowing.

(3) put it in context---the EU is going into double (triple?) dip recession---the US is in the worst recovery ever, and seems to be slowing even more now, and the rest of the BRICs aren't doing too great either.

I sold out of the stock market a couple of weeks ago when the EU stole people's bank deposits in Cyprus. It reminded me of the collapse of Bear Stearns and other small but completely irrational financial disasters that sometimes presage even bigger disasters. I thought the appearance of that kind of government criminality a very bad sign for the EU, and now they are talking in the EU about "wealth taxes"---just seizing people's property anywhere in the EU. Since I'm out of the market I'm now a bit biased and predisposed to look for more bad signs in the global economy. I take the slowing in China as yet another bad sign.

But

(1) you can't trust the Chinese data----if the government is reporting growth has to slowed to under 8% it might well be quite a bit worse.

(2) the "trend is not your friend here"---growth in China is definitely slowing.

(3) put it in context---the EU is going into double (triple?) dip recession---the US is in the worst recovery ever, and seems to be slowing even more now, and the rest of the BRICs aren't doing too great either.

I sold out of the stock market a couple of weeks ago when the EU stole people's bank deposits in Cyprus. It reminded me of the collapse of Bear Stearns and other small but completely irrational financial disasters that sometimes presage even bigger disasters. I thought the appearance of that kind of government criminality a very bad sign for the EU, and now they are talking in the EU about "wealth taxes"---just seizing people's property anywhere in the EU. Since I'm out of the market I'm now a bit biased and predisposed to look for more bad signs in the global economy. I take the slowing in China as yet another bad sign.

-

Plantagenet - Expert

- Posts: 26628

- Joined: Mon 09 Apr 2007, 03:00:00

- Location: Alaska (its much bigger than Texas).

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by ROCKMAN » Mon 15 Apr 2013, 14:10:26

by ROCKMAN » Mon 15 Apr 2013, 14:10:26

P – I’m with you. Got out of the market and sunk all my savings into this really hot tapioca mine investment. LOL. Actually about to make one of the better investments I have in front of me: paying off the home mortgage. Given the low rates not for everyone but I have some unique circumstances.

Whatever the US economic future may be it just feels like we’re sliding off long term to a place we’ve never been at least in my lifetime. Not just PO and perhaps even more than my more inclusive POD…Peal Oil Dynamic. Maybe PE…Peak Economies. Or PIA…Peak Industrial Age. I now that may sound a tad over the top but I’ve been aware of PO for almost 4 decades and have seen the signs of it for that long. But matters feel much different to me these days. Or maybe I’m just getting too old and worn out. LOL.

Whatever the US economic future may be it just feels like we’re sliding off long term to a place we’ve never been at least in my lifetime. Not just PO and perhaps even more than my more inclusive POD…Peal Oil Dynamic. Maybe PE…Peak Economies. Or PIA…Peak Industrial Age. I now that may sound a tad over the top but I’ve been aware of PO for almost 4 decades and have seen the signs of it for that long. But matters feel much different to me these days. Or maybe I’m just getting too old and worn out. LOL.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by Econ101 » Mon 15 Apr 2013, 18:25:11

by Econ101 » Mon 15 Apr 2013, 18:25:11

8% growth in China is very good. They have been at abnormal growth levels for many years as they expanded into their capacity with a vicious wage/price war on the rest of the world. For a young, growing economy those numbers were normal. China is bigger than normal too so abnormal growth lasted a lot longer than normal.

Now they are maturing as a manufacturing and trade economy. They have shown the world the greatest gift to humanity in history. That economy, once it adopted capitalists principals, has lifted a billion people out of terrible, suffering poverty, into a new existence where happiness and security can replace fear and hunger. Their government however, is still too heavy handed.

As a mature economy their growth will slow similar to ours. They will begin to export work they have in excess. Others will then benefit from that. Its all a very good thing and happening right before our eyes.

Now they are maturing as a manufacturing and trade economy. They have shown the world the greatest gift to humanity in history. That economy, once it adopted capitalists principals, has lifted a billion people out of terrible, suffering poverty, into a new existence where happiness and security can replace fear and hunger. Their government however, is still too heavy handed.

As a mature economy their growth will slow similar to ours. They will begin to export work they have in excess. Others will then benefit from that. Its all a very good thing and happening right before our eyes.

- Econ101

- Lignite

- Posts: 322

- Joined: Sat 01 Sep 2012, 07:47:56

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by SeaGypsy » Mon 15 Apr 2013, 23:48:06

by SeaGypsy » Mon 15 Apr 2013, 23:48:06

Pretty pathetic that the world is now so hinged on Chinese growth that a .2% drop in expectation is enough to trigger a global market slump.

- SeaGypsy

- Master Prognosticator

- Posts: 9285

- Joined: Wed 04 Feb 2009, 04:00:00

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by seahorse3 » Wed 17 Apr 2013, 11:51:32

by seahorse3 » Wed 17 Apr 2013, 11:51:32

We've all talked/preached for a long time that the world can't have economic growth (ak GDP growth) without oil production growth. But, are there any charts on that? Any charts that show oil production growth on a world wide basis with world GDP growth? Obviously oil production went gangbusters up to about 2005 and has increased some since then, but not enough to keep the illusion of economic BAU going. So, if there is a chart please link.

This leads to problem no. 2, when oil production goes flat, and GDP goes flat, it means the current system of "globalization" for everyone doesn't work. We need a new model. That model used the dollar as the reserve currency. That model assumed we could all grow and benefit together. Now, we can't. So, China to maintain its growth will cut deals to get what oil is there - we see that happening. We see China now negotiating deals to get the yuan accepted in trade deals and away from the dollar. So, the old model is changing or breaking down. Under the old model, we see bankers taking deposits in Cyprus. So, banks no longer make money by lending, but by charging fees and taking creditor deposits. Look at American banks. Under the old growth model, when growth was possible while oil production was rising, they made money the traditional way by lending. Now, over the last few years, they are making money off of fees, aka things like overdraft fees. So, the old system is changing. I believe its due to a stall in oil production, meaning no growth, meaning old system will change. Into what? Who knows. But the old assumptions have to go away.

On a personal note, I too believe the best investment is always investing in yourself, meaning get debt free. Then, if you have extra money, sock away enough to survive at least a year on; then, if you have anything left, "invest" it.

This leads to problem no. 2, when oil production goes flat, and GDP goes flat, it means the current system of "globalization" for everyone doesn't work. We need a new model. That model used the dollar as the reserve currency. That model assumed we could all grow and benefit together. Now, we can't. So, China to maintain its growth will cut deals to get what oil is there - we see that happening. We see China now negotiating deals to get the yuan accepted in trade deals and away from the dollar. So, the old model is changing or breaking down. Under the old model, we see bankers taking deposits in Cyprus. So, banks no longer make money by lending, but by charging fees and taking creditor deposits. Look at American banks. Under the old growth model, when growth was possible while oil production was rising, they made money the traditional way by lending. Now, over the last few years, they are making money off of fees, aka things like overdraft fees. So, the old system is changing. I believe its due to a stall in oil production, meaning no growth, meaning old system will change. Into what? Who knows. But the old assumptions have to go away.

On a personal note, I too believe the best investment is always investing in yourself, meaning get debt free. Then, if you have extra money, sock away enough to survive at least a year on; then, if you have anything left, "invest" it.

- seahorse3

- Lignite

- Posts: 375

- Joined: Tue 01 Mar 2011, 16:14:13

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by Tanada » Wed 17 Apr 2013, 14:57:03

by Tanada » Wed 17 Apr 2013, 14:57:03

seahorse3 wrote:We've all talked/preached for a long time that the world can't have economic growth (ak GDP growth) without oil production growth. But, are there any charts on that? Any charts that show oil production growth on a world wide basis with world GDP growth? Obviously oil production went gangbusters up to about 2005 and has increased some since then, but not enough to keep the illusion of economic BAU going. So, if there is a chart please link.

I have argued more or less since I got here that Energy use goes up with GDP growth but not necessarily oil energy. Fission, Solar, Wind, Hydro, heck even Coal and Natural Gas can substitute for Oil use in different energy uses. You can build a ship that uses Fission or Coal as its driving force, or even wind like we did before Steam came along. You could still build coal fired steam locomotives today if you want to stop buying diesel fueled locomotives. My understanding is the PRC still runs a ferw dozen coal fired steam engines even in 2013.

Alfred Tennyson wrote:We are not now that strength which in old days

Moved earth and heaven, that which we are, we are;

One equal temper of heroic hearts,

Made weak by time and fate, but strong in will

To strive, to seek, to find, and not to yield.

-

Tanada - Site Admin

- Posts: 17059

- Joined: Thu 28 Apr 2005, 03:00:00

- Location: South West shore Lake Erie, OH, USA

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by EdwinSm » Tue 04 Jun 2013, 00:06:10

by EdwinSm » Tue 04 Jun 2013, 00:06:10

Bump...

http://www.bbc.co.uk/news/business-22754725

China still has a high rate of growth, but news like this implies that that will slow down. Will jobs come back to Europe or North America?

China: 'Scary' pace of change prompts investor rethink.

For the past 20 years, Taiwanese businessman Jimmy Chu, the head of a company that makes elevators and forklifts, has been spending most of his investments, and time, in mainland China.

Some 80,000 Taiwanese companies like Mr Chu's have poured a total of $120bn into the country in the past two decades, making Taiwan one of the biggest investors there and a key driver of China's economic growth.

But Mr Chu will soon open two new factories in Taiwan at a total investment of $70m, the biggest he has made at home in years.

He is among an increasing number of Taiwanese shifting at least some of their operations away from China - either to South East Asia or Taiwan - and adjusting their investment strategies in the mainland.

One of the main reasons is a significant rise in Chinese wages. Some estimate salaries have doubled in the past six to seven years. Companies are also now required to pay into Chinese workers' health insurance and pension plans.

"Labour costs in China are rising dramatically each year and the pace is scary," says Mr Chu, chief executive of Fair Friend Enterprise Group.

http://www.bbc.co.uk/news/business-22754725

China still has a high rate of growth, but news like this implies that that will slow down. Will jobs come back to Europe or North America?

- EdwinSm

- Tar Sands

- Posts: 601

- Joined: Thu 07 Jun 2012, 04:23:59

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by ROCKMAN » Tue 04 Jun 2013, 08:24:46

by ROCKMAN » Tue 04 Jun 2013, 08:24:46

pstarr - I get the idea but really: "stuck"? LOL. Macro-economics aren't my thing but I clearly recall the days when many were warning that China's 10%+ growth was dangerous with regards to their future stability. Based upon those thoughts Chinese growth slowing down a tad should be positive news.

Well, back to work for me now. Let me tell you it's a real pain in the ass to be 'stuck' with a portion of the profits when we flip the company in a couple of years. Poor lil' me...and China too. Boo hoo hoo. LOL.

Well, back to work for me now. Let me tell you it's a real pain in the ass to be 'stuck' with a portion of the profits when we flip the company in a couple of years. Poor lil' me...and China too. Boo hoo hoo. LOL.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by Arthur75 » Tue 04 Jun 2013, 08:55:53

by Arthur75 » Tue 04 Jun 2013, 08:55:53

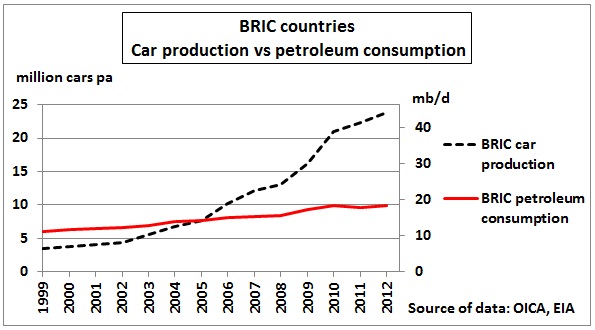

About China, interesting analyis from Matt Mushalik, about the number of cars and oil usage in the world :

This is for the BRICS but China a major part of it :

Using the same ratio of petroleum consumption to car production as in the non-BRIC graph above we see that cars before 2005 were under-produced and after that over-produced. The trend line of car production and petroleum consumption have completely different directions, meaning that BRIC cars are driven less. If that should change, there would be an unbridgeable gap in oil production of more than 25 mb/d

This is for the BRICS but China a major part of it :

-

Arthur75 - Tar Sands

- Posts: 529

- Joined: Sun 29 Mar 2009, 05:10:51

- Location: Paris, France

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by John_A » Tue 04 Jun 2013, 09:02:31

by John_A » Tue 04 Jun 2013, 09:02:31

pstarr wrote:We have no chance of retooling anymore. We have no chance of installing adequate rail freight, commuter rail lines, or even bike lanes.

???

Was riding on a few new ones just last week. Do you mean we will run out of the political will to dedicate the shoulder of the road to us bicyclists, or that peak oil will somehow cause a lack of paint?

45ACP: For when you want to send the very best.

- John_A

- Heavy Crude

- Posts: 1193

- Joined: Sat 25 Jun 2011, 21:16:36

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by kublikhan » Tue 04 Jun 2013, 12:09:49

by kublikhan » Tue 04 Jun 2013, 12:09:49

Some jobs will come back. Not just because of labor costs, but high fuel costs are biting into companies trying to ship products half way around the world. "offshoring" is still more dominant than "reshoring", but offshoring is no longer as dominant as it once was and the trend is shifting a bit.EdwinSm wrote:China still has a high rate of growth, but news like this implies that that will slow down. Will jobs come back to Europe or North America?

Here, there and everywhereEARLY NEXT MONTH local dignitaries will gather for a ribbon-cutting ceremony at a facility in Whitsett, North Carolina. A new production line will start to roll and the seemingly impossible will happen: America will start making personal computers again. Mass-market computer production had been withering away for the past 30 years, and the vast majority of laptops have always been made in Asia. Dell shut two big American factories in 2008 and 2010 in a big shift to China, and HP now makes only a small number of business desktops at home.

The new manufacturing facility is being built not by an American company but by Lenovo, a highly successful Chinese technology group. Lenovo’s move marks the latest twist in a globalisation story that has been running since the 1980s.

The first and most important reason is that the global labour “arbitrage” that sent companies rushing overseas is running out. Wages in China and India have been going up by 10-20% a year for the past decade, whereas manufacturing pay in America and Europe has barely budged. Other countries, including Vietnam, Indonesia and the Philippines, still offer low wages, but not China’s scale, efficiency and supply chains. There are still big gaps between wages in different parts of the world, but other factors such as transport costs increasingly offset them. Lenovo’s labour costs in North Carolina will still be higher than in its factories in China and Mexico, but the gap has narrowed substantially, so it is no longer a clinching reason for manufacturing in emerging markets. With more automation, says David Schmoock, Lenovo’s president for North America, labour’s share of total costs is shrinking anyway.

Second, many American firms now realise that they went too far in sending work abroad and need to bring some of it home again, a process inelegantly termed “reshoring”. Well-known companies such as Google, General Electric, Caterpillar and Ford Motor Company are bringing some of their production back to America or adding new capacity there. In December Apple said it would start making a line of its Mac computers in America later this year.

Firms are now discovering all the disadvantages of distance. The cost of shipping heavy goods halfway around the world by sea has been rising sharply, and goods spend weeks in transit. They have also found that manufacturing somewhere cheap and far away but keeping research and development at home can have a negative effect on innovation. One answer to this would be to move the R&D too, but that has other drawbacks: the threat of losing valuable intellectual property in far-off places looms ever larger. And a succession of wars and natural disasters in the past decade has highlighted the risk that supply chains a long way from home may become disrupted.

Third, firms are rapidly moving away from the model of manufacturing everything in one low-cost place to supply the rest of the world. China is no longer seen as a cheap manufacturing base but as a huge new market. Increasingly, the main reason for multinationals to move production is to be close to customers in big new markets. This is not offshoring in the sense the word has been used for the past three decades; instead, it is being “onshore” in new places.

Companies now want to be in, or close to, each of their biggest markets, making customised products and responding quickly to changing local demand. Lenovo, as a Chinese company, has its own factories in China. The reason it is moving some production to America is that it will be able to customise its computers for American customers and respond quickly to them. If it made them in China they would spend six weeks on a ship, says Mr Schmoock.

Under this logic, America and Europe, with their big domestic markets, should be able to attract plenty of new investment as companies look for a bigger local presence in places around the world. It is not just Western firms bringing some of their production home; there is also a wave of emerging-market champions such as Lenovo, or the Tata Group, which is making Range Rover cars near Liverpool, that are coming to invest in brands, capacity and workers in the West.

Such changes are happening not only in manufacturing but increasingly in services too. Companies may either outsource IT and back-office work to other companies, which could be in the same country or abroad, or offshore it to their own centres overseas. Software programming, call centres and data-centre management were the first tasks to move, followed by more complex ones such as medical diagnoses and analytics for investment banks.

As in manufacturing, the labour-cost arbitrage in services is rapidly eroding, leaving firms with all the drawbacks of distance and ever fewer cost savings to make up for them. There has been widespread disappointment with outsourcing information technology and the routine back-office tasks that used to be done in-house. Some activities that used to be considered peripheral to a company’s profits, such as data management, are now seen as essential, so they are less likely to be entrusted to a third-party supplier thousands of miles away.

The oil barrel is half-full.

-

kublikhan - Master Prognosticator

- Posts: 5023

- Joined: Tue 06 Nov 2007, 04:00:00

- Location: Illinois

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by furrybill » Tue 04 Jun 2013, 12:44:08

by furrybill » Tue 04 Jun 2013, 12:44:08

I read about China manufacturing dipping and other things like gold going down, tame inflation, jobless rates not moving and I begin to wonder: Could a Japanese-style lost decade, deflationary period be in the near future for the entire world? Were the first few years of the 2000's such a run up, such a bubble that we really needed a severe crash to correct? And since that didn't happen and instead we're printing money we're just going to limp along for many years?

-

furrybill - Peat

- Posts: 101

- Joined: Thu 28 Feb 2008, 04:00:00

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by EdwinSm » Tue 25 Jun 2013, 01:34:42

by EdwinSm » Tue 25 Jun 2013, 01:34:42

China stocks enter bear market amid credit fears

Chinese stocks have fallen further amid continued concern over the impact of a credit tightening on its economy.

The Shanghai Composite SSE index fell 3.8% to 1,888.68 points, entering the bear market territory, often described as a 20% dip from the recent peak.

The index has dipped 23% since its high of 2,444.80 points in February.

The concern came after the central bank indicated its credit-tightening policy would continue, saying that the era of cheap cash was over.

....

In recent days the People's Bank of China (PBOC), the country's central bank, temporarily turned off the flow of cheap money in an attempt to impose more discipline on its banks and reduce their reliance on credit.

That resulted in China's banks - mostly state-owned - charging each other some of the highest lending rates ever - over 25% in some cases - triggering fears of a credit crunch.

....

"In fact, the central bank wants to root out the poorly-performing banks - especially those in the so-called shadow banking system."

......

Analysts and investors have been concerned that if growth in China slows sharply, it will impact growth in the region's economies that rely on Chinese demand.

.....

http://www.bbc.co.uk/news/business-23041912

This seems to be like slamming on the brakes - 23% fall in stock market, inter-bank interest rates hitting 25%, and expectation that banks will fail. While pointing to the changes expected to be seen when QE comes to an end, will the more gradual tappering off be seen more like a gentle application of the brakes and so the prevent the extreme reactions seen in China?

Will this mean that the adverts that pop up on this site trying to sell me "Made in China" goods will change to selling me a "Maid from China"?

- EdwinSm

- Tar Sands

- Posts: 601

- Joined: Thu 07 Jun 2012, 04:23:59

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by dolanbaker » Tue 25 Jun 2013, 02:57:24

by dolanbaker » Tue 25 Jun 2013, 02:57:24

Even if Chinese growth flatlines, it is still twice the size it was a decade ago and consuming/ producing twice what it used to.

Ultimately, Chinese "growing space" will be determined by the availability of resources not consumed by the western countries that are currently declining.

Every barrel of oil not consumed by countries like Ireland is being redirected to China, but barring another economic crisis the decline in consumption (in Ireland) will level off, thus reducing the "growth" in supply to China.

Ultimately, Chinese "growing space" will be determined by the availability of resources not consumed by the western countries that are currently declining.

Every barrel of oil not consumed by countries like Ireland is being redirected to China, but barring another economic crisis the decline in consumption (in Ireland) will level off, thus reducing the "growth" in supply to China.

Religion is regarded by the common people as true, by the wise as false, and by rulers as useful.:Anonymous

Our whole economy is based on planned obsolescence.

Hungrymoggy "I am now predicting that Europe will NUKE ITSELF sometime in the first week of January"

Our whole economy is based on planned obsolescence.

Hungrymoggy "I am now predicting that Europe will NUKE ITSELF sometime in the first week of January"

-

dolanbaker - Intermediate Crude

- Posts: 3855

- Joined: Wed 14 Apr 2010, 10:38:47

- Location: Éire

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by ROCKMAN » Tue 25 Jun 2013, 08:05:23

by ROCKMAN » Tue 25 Jun 2013, 08:05:23

db – Good point about the size of China but they are a long way from flat lining IMHO. In fact, in a another thread I referred to a story that by the govt increasing the overnight interest rates they have probably gone a long way towards stabilizing the economy and aided slower BUT sustained long term steady economic growth.

And assuming there’s a correlation between economic growth and energy consumption this also infers long term and stable growth in energy consumption. As far as “the decline in consumption (in Ireland) will level off, thus reducing the "growth" in supply to China” I don’t see the dynamic moving that way. China won’t be getting what energy is left after other countries have their fill IMHO. In one manner or another China is tying up huge volumes of future energy production. Ireland et al will acquire what energy that’s available that they can afford. In addition to a significant amount of capital to buy reserves China has long term supply commitments from numerous exporters. Does Ireland have even 1 bopd committed long term from any of their exporting supply sources? I’m not 100% sure but I don’t think so. Ireland, as well as many of the countries around the world, will only be able to acquire what energy is available in the open market…if they can afford it. Starting in 2003 Ireland increased the cost of their oil imports by 400% in just 5 years. Today they reduced that amount by 25% from their peak. It remains to be seen if Ireland ever again imports as much as they did in 2008. They may be recovering from their economic bust but that, in and of itself, doesn’t mean they’ll ever have the ability to import that much oil again. It may not be available or, if available, not affordable.

A country’s demand doesn’t determine what energy they can acquire. And PO doesn’t mean everyone will share the lack of energy equally. In the case of China their concern isn’t global peak oil. It China’s peak imports. Which, for the moment, looks like they’ve handled well. Ireland (and many other countries) may be at or past their individual peak import. If so their growth potential will likely be controlled by this factor. And that doesn’t bode well for many of the world’s economies IMHO.

And assuming there’s a correlation between economic growth and energy consumption this also infers long term and stable growth in energy consumption. As far as “the decline in consumption (in Ireland) will level off, thus reducing the "growth" in supply to China” I don’t see the dynamic moving that way. China won’t be getting what energy is left after other countries have their fill IMHO. In one manner or another China is tying up huge volumes of future energy production. Ireland et al will acquire what energy that’s available that they can afford. In addition to a significant amount of capital to buy reserves China has long term supply commitments from numerous exporters. Does Ireland have even 1 bopd committed long term from any of their exporting supply sources? I’m not 100% sure but I don’t think so. Ireland, as well as many of the countries around the world, will only be able to acquire what energy is available in the open market…if they can afford it. Starting in 2003 Ireland increased the cost of their oil imports by 400% in just 5 years. Today they reduced that amount by 25% from their peak. It remains to be seen if Ireland ever again imports as much as they did in 2008. They may be recovering from their economic bust but that, in and of itself, doesn’t mean they’ll ever have the ability to import that much oil again. It may not be available or, if available, not affordable.

A country’s demand doesn’t determine what energy they can acquire. And PO doesn’t mean everyone will share the lack of energy equally. In the case of China their concern isn’t global peak oil. It China’s peak imports. Which, for the moment, looks like they’ve handled well. Ireland (and many other countries) may be at or past their individual peak import. If so their growth potential will likely be controlled by this factor. And that doesn’t bode well for many of the world’s economies IMHO.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by kublikhan » Tue 25 Jun 2013, 13:37:46

by kublikhan » Tue 25 Jun 2013, 13:37:46

+1ROCKMAN wrote:And assuming there’s a correlation between economic growth and energy consumption this also infers long term and stable growth in energy consumption. As far as “the decline in consumption (in Ireland) will level off, thus reducing the "growth" in supply to China” I don’t see the dynamic moving that way. China won’t be getting what energy is left after other countries have their fill IMHO.

I think you have it backwards db. IMHO, developing countries will be the ones determining oil demand growth and developed countries will see their oil consumption continue to shrink. Developing nations derive a much higher marginal utility for every barrel of oil they consume.

Growth challenges in developed economiesWhy are developing countries managing to grow rapidly, even at double digit rates, while developed countries cannot manage to achieve any meaningful growth?

The answer lies primarily in global resource and environmental constraints. An overcrowded planet and massive industrialization of developing countries have brought mankind face to face with the limits of the planet. These limits tend to constrain global economic growth.

In the following pages we will examine the ways these resource and environmental constraints work their way through the global economy and the effects they have on its developed and developing segments. Since the growth challenges we are concerned about mainly emanate from resource and environmental constraints it is important to mention that an important difference between developed and developing economies is their resource intensiveness. This discussion is mainly about the resource intensiveness of developed and developing economies and the resulting growth challenges they face.

A more than 1000 percent increase in the price of oil in the recent decade, or so, has seriously affected most developed economies. It has rendered unviable a wide range of economic activities that previously made sense. All sectors of the economy including energy, transportation, housing, recreation and tourism, and retail are affected.

The same is not the case with developing countries. Low oil consumption in developing countries helps them keep their costs low, including wages. Developing countries wages are somewhat immune from oil price hikes. Business and economic activities suffer relatively little from oil price hikes in developing countries. Developing economies do not generally go into an economic recession due to oil price hikes. Their economic growth continues in spite of oil price hikes.

Economic growth is fast becoming a zero-sum game among countries because of fossil fuel supply constraint and the likely consequences of environmental constraints. Since resource limits will not allow the global economy to grow freely; growth in developing countries will exert offsetting downward pressure on growth in developed countries. Growth in developing countries will come at the cost of growth in developed countries. Migration of industries without replacement is just one example.

Utility maximization from oil

Assuming that the world is a consumer with a finite amount of oil; it will try to maximize its utility by equalizing the marginal utility from all its different uses of oil. Globalization has helped create conditions where the world is like a consumer trying to maximize its utility from scarce resources. In other words the global economy is trying to equalize its utility from oil use in all parts of the world.

Global utility maximization is working through resource, labor, end product and other prices, to equalize the utility derived from oil use in different parts of the world. Global utility maximization currently translates into reducing resource use in developed countries and increasing it in developing countries. This market pressure to reduce fossil fuel use in developed countries may be called a “market driven correction” but in real life it is the economic crisis!

Globalization and the resultant massive industrialization of developing countries brought two billion people in the global workforce. Consequently, a large number of businesses in developed economies are facing tough low wage competition from developing economies. As a result they are either closing down or moving to developing countries to take advantage of their low wages. When businesses move overseas they not only take the employment and income that they created but also the opportunities and the potentials that they created for other businesses; they take an additional piece of the economy with them.

Growing Competitive Disadvantage of Developed Economies

Almost all production and consumption activity in developed countries has a significant component of oil or energy use. Due to high and ubiquitous usage of fossil fuel, the cost structures in developed countries get pushed up higher by oil price hikes. Wage standards are also pushed up or lose downward flexibility because of oil price hikes, particularly given the cumulative effect of hikes in the recent decade. Therefore competitive abilities of business in developed countries tend to be diminished by oil price hikes and related expectations.

In developing countries, on the other hand, oil price hikes do not significantly affect wages and other costs due to their low usage of fossil fuel. Low intensity of energy use also helps them keep wages low. Due to low intensity of energy use in developing countries their costs do not go up as much by oil price hikes as they do in developed countries. The economic effects of oil price hikes are many times higher in developed countries than in developing ones. Developing countries gain some competitive advantage over developed countries every time oil price increases.

Global resource constraints, i.e. rising oil prices, have put developed countries at a significant and increasing disadvantage vis-à-vis developing countries. If developed countries continue on the fossil fuel path they will keep losing jobs and business to developing countries.

Oil buying power of developing countries

Since consumers in developing countries have a low rate of oil consumption, they are likely to derive higher marginal utility from consumption of oil compared to that in developed countries. Therefore consumers in developing countries are more likely to be willing to pay for rising oil prices. Oil consumption in developing countries will keep pressure on oil prices.

It may seem that developed countries have more buying power, but for oil and similar global resources, the production and consumption economics favor developing countries and give them better buying power. Since oil price hikes do not significantly affect wages, only direct costs have to be transferred to end products in developing countries. Direct costs are easy to transfer to end product prices. Oil price hikes are easier to deal with there.

Developed countries have built their economies on oil prices of around $10, or $20, a barrel whereas developing countries are building theirs on $100 a barrel. Developing countries therefore are able to deal with high oil prices without much pain or restructuring.

Developing countries’ growth is likely to continue in spite of rising oil and other resource prices. The same cannot be said about developed countries. Because of high intensity of energy and oil use developed economies will be increasingly crippled by rising oil prices.

The oil barrel is half-full.

-

kublikhan - Master Prognosticator

- Posts: 5023

- Joined: Tue 06 Nov 2007, 04:00:00

- Location: Illinois

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by dolanbaker » Tue 25 Jun 2013, 16:53:50

by dolanbaker » Tue 25 Jun 2013, 16:53:50

kublikhan wrote:+1ROCKMAN wrote:And assuming there’s a correlation between economic growth and energy consumption this also infers long term and stable growth in energy consumption. As far as “the decline in consumption (in Ireland) will level off, thus reducing the "growth" in supply to China” I don’t see the dynamic moving that way. China won’t be getting what energy is left after other countries have their fill IMHO.

I think you have it backwards db. IMHO, developing countries will be the ones determining oil demand growth and developed countries will see their oil consumption continue to shrink. Developing nations derive a much higher marginal utility for every barrel of oil they consume.

Yes, I agree that will be the case in the future, I was really thinking about the recent past where the decline in consumption greatly benefited China.

Religion is regarded by the common people as true, by the wise as false, and by rulers as useful.:Anonymous

Our whole economy is based on planned obsolescence.

Hungrymoggy "I am now predicting that Europe will NUKE ITSELF sometime in the first week of January"

Our whole economy is based on planned obsolescence.

Hungrymoggy "I am now predicting that Europe will NUKE ITSELF sometime in the first week of January"

-

dolanbaker - Intermediate Crude

- Posts: 3855

- Joined: Wed 14 Apr 2010, 10:38:47

- Location: Éire

Re: CHINA STUCK WITH SUB-8% GROWTH

![]() by Tanada » Tue 25 Jun 2013, 22:39:46

by Tanada » Tue 25 Jun 2013, 22:39:46

I think the PRC is deliberately slowing their rate of growth because they do not want the citizens to get into the whole bubble creation cycle the west is so famous for. Even a 2% growth rate would exceed their population needs, after all how much percentage of the Chinese population do they want to own a private car? If you put 500,000,000 cars and SUV's on the road network you will grossly overwhelm the systems in place. The infrastructure and culture needs to catch up to what is practical and possible instead of what Hollywood says they should want.

Alfred Tennyson wrote:We are not now that strength which in old days

Moved earth and heaven, that which we are, we are;

One equal temper of heroic hearts,

Made weak by time and fate, but strong in will

To strive, to seek, to find, and not to yield.

-

Tanada - Site Admin

- Posts: 17059

- Joined: Thu 28 Apr 2005, 03:00:00

- Location: South West shore Lake Erie, OH, USA

28 posts

• Page 1 of 2 • 1, 2

Who is online

Users browsing this forum: No registered users and 9 guests