Here's How You Can Profit From the United States' Oil Boom:

http://www.fool.com/investing/general/2 ... es-oi.aspx

Photo caption for the article says it all:

“Saudi Arabia can keep its oil, we have enough of our own.”

A trip down memory lane. . .

EIA data show that Alaska's crude oil production (C+C) increased from 0.17 mbpd in 1976 to 2.0 mbpd in 1988 (as production from the North Slope came on line via the Trans-Alaskan Pipeline). This was a 20%/year rate of increase. At this rate of increase in Alaskan crude oil production, the US would have been crude oil self-sufficient in about 7 years, around the year 1995. Of course, reality intervened, and Alaskan crude oil production fell from 2.0 mbpd in 1988 to 1.5 mbpd in 1995, a rate of decline of 4%/year.

And today . . .

Assuming an average annual US crude oil production rate of about 7.5 mbpd in 2013, at the 2008 to 2013 rate of increase in US crude oil production, 8%/year, the US would be approximately crude oil self-sufficient in about 9 years, around the year 2022. On a net imports basis (based on total liquids and current data), we would actually achieve zero net liquids imports prior to 2022, probably around the 2020 mark that has been frequently mentioned.

So, either declines from discrete producing regions like the North Slope of Alaska are inevitable, or the laws of nature have been repealed.

It's pretty clear what the conventional wisdom is these days, as we see virtually daily headlines proclaiming that the Peak Oil "Theory" is dead. The logical conclusion one can draw from this proclamation is that the finite sum of discrete producing regions, like the North Slope, that peak and decline will result in a virtually perpetual rate of increase in production.

For an alternative (reality based) point of view, following is a link to, and excerpt from, a recent essay I wrote:

Commentary: Is it only a question of when the US once again becomes a net oil exporter?

http://www.resilience.org/stories/2013- ... l-exporter

We are currently processing about 15 million b/d of crude oil in US refineries (actually 16 mbpd in July, 2013). A portion of the refined product is exported, and then we have refinery gains plus biofuels plus natural gas liquids, but let's ignore all of that and focus on crude oil production versus refinery inputs. Currently, we are producing about half of the crude oil inputs into US refineries, and importing the other half.

If we want to produce, in 2023, 100% of the crude oil that we currently process in US refineries, based on the above assumptions (especially a 10 percent /year decline rate), we would need to add the 7.5 million b/d, in order to offset declines, plus add another 7.5 million b/d over 10 years, for a total of 15 million b/d of new production, or about 1.5 million b/d per day per year for 10 years. And of course, once we reach the 15 million b/d level, assuming a 10%/year decline rate, we would need 1.5 million b/d of new production, every year, just to maintain the 15 million b/d production rate.

To meet the 1.5 million b/d per year rate, in order to be crude oil independent by 2023, in round numbers we would need to add--every single year--the combined current productive equivalent of the Bakken Play + the Eagle Ford Play. Or, we would need to add, over 10 years, the productive equivalent of the 2012 crude oil production from Saudi Arabia + Iraq + Kuwait.

This exercise illustrates why peaks happen, and it shows why production declines are inevitable. On the upslope of a production increase, new oil wells can offset the declines from existing wellbores, but with time, new oil wells can no longer offset the increasing volume of oil lost to production declines.

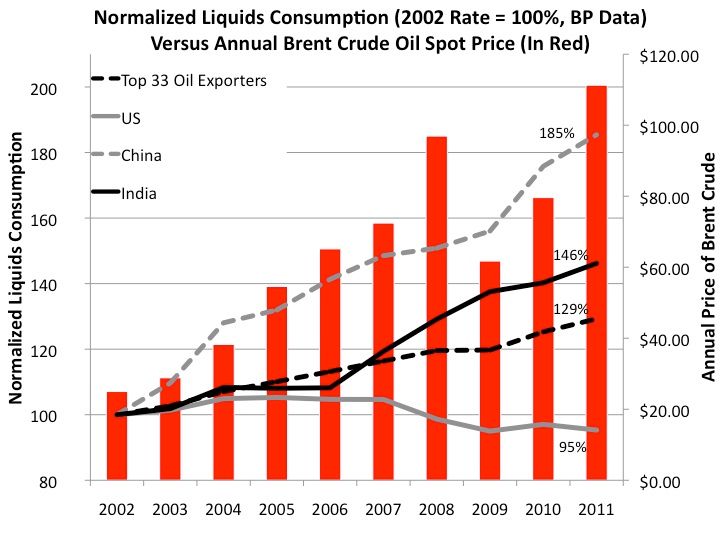

In reality, what the data show--at least through 2012--is that developed net oil importing countries like the US were gradually being shut out of the global market for exported oil, via price rationing, as developing countries, led by China, consumed an increasing share of a post-2005 declining volume of Global Net Exports of oil.