Economics: Account for depreciation of natural capital

For the past year, academics and policy-makers have been discussing Thomas Piketty's 2013 economics best-seller, Capital in the Twenty-First Century1. It documents the considerable rise over the past 40 years in national wealth relative to national income in eight of the richest economies — the United States, Japan, Germany, France, the United Kingdom, Italy, Canada and Australia. The national wealth of each of these countries increased from 2–3 times national income in 1970 to 4–6 times income in 2010.

Piketty relies on standard income conventions as prescribed in the United Nations national accounts. He includes natural resources such as fossil fuels, minerals and forests in his estimate of a country's capital. But his measures of national income and savings adjust only for depreciation of 'fixed capital' — buildings, equipment and so on.

We must also account for the depreciation of natural capital in appraising wealth. This is the value of net losses to natural resources, such as minerals, fossil fuels, forests and similar sources of material and energy inputs into our economy. If we use up more natural capital to produce economic output today, then we have less for production tomorrow.

At the same time, we are also squandering valuable ecological capital — ecosystems provide important goods and services to the economy, such as recreation, flood protection, nutrient uptake, erosion control, water purification and carbon sequestration. By converting and degrading ecosystems, we are depreciating this important ecological capital endowment.

Economic indicators change dramatically when the depletion and degradation of natural resources and ecosystems are accounted for. Here, I show by how much, through a worked example of mangroves in Thailand. Depreciation of natural capital is particularly high in developing economies, which are often rich in resources and ecosystems. We must retool our measures of income and wealth accordingly, starting with net domestic product.

Creative accounting

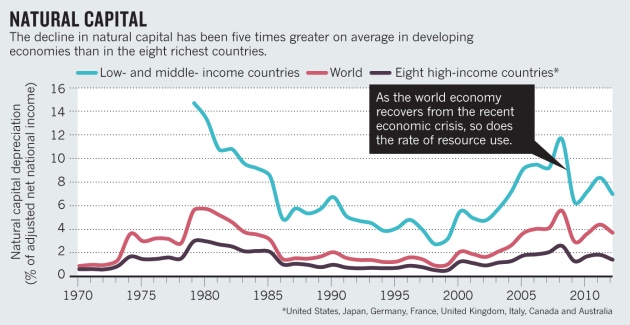

Since 1970, the World Bank's World Development Indicators have provided estimates for most countries of the adjustments to national income, income growth and savings that arise from net depletion of forests, energy resources and minerals. This rate of natural-capital depreciation as a percentage of adjusted net national income over the past four decades is alarming (see 'Natural capital').

Two global trends are noticeable. First, the decline in natural capital has been five times greater on average in developing economies than in the eight richest countries. Second, natural capital depreciation in all countries has risen significantly since the 1990s. There was a dip during the global recession of 2008–09, but as the world economy has recovered, so has the rate of resource use.

Ecological capital, too, is clearly endangered by current patterns of economic development. Over the past 50 years, ecosystems have been modified more rapidly and extensively than in any comparable period in human history, largely to meet burgeoning demands for food, fresh water, timber, fibre and fuel. According to the worldwide Millennium Ecosystem Assessment, approximately 60% of major global ecosystem services have been degraded or used unsustainably, including fresh water, wild fisheries, air and water purification, and the regulation of regional and local climate, natural hazards and pests.

Unfortunately, ecological capital, being unique, poorly understood and difficult to measure, tends to be undervalued. Consider the example of mangroves in Thailand from 1970 to 20092. Average annual mangrove loss in Thailand has fallen steadily in every decade since the 1970s. Yet cumulatively, Thailand is estimated to have lost around one-third of its mangroves since the 1970s, mainly to the expansion of shrimp farming and other coastal development.

Natural Capital