I was going to make a new thread, but this one seems appropriate. First of all, this is the problem:

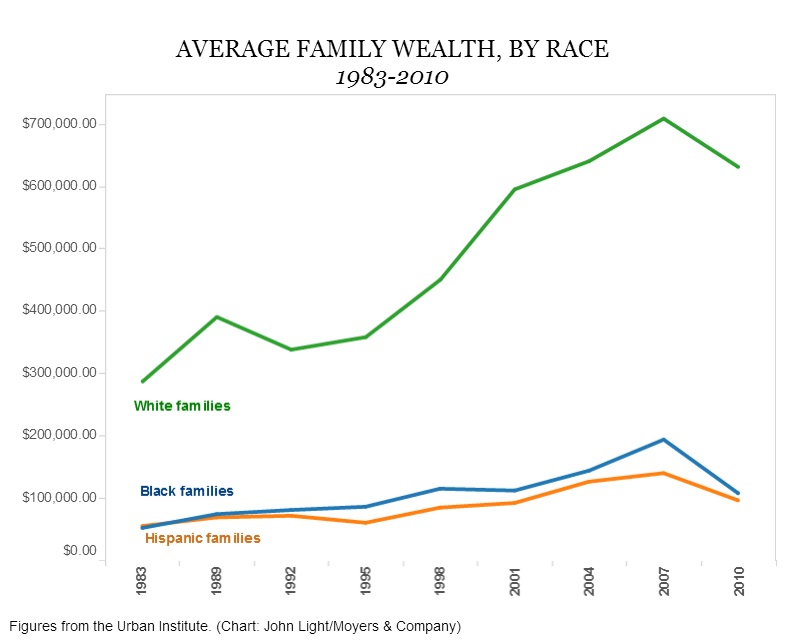

Just since 1989, surely within the lifespans of most of us, the family wealth gap, measured by race, has drastically increased. Note in the chart above that average white families have about $650,000, while Blacks and Latinos have less than a quarter of that.

The above chart leaves out an important point, which is that most families also have debt, mainly mortgage debt, sometimes credit debt, from charge cards or education loans. When you measure net wealth ((Savings + Assets) - Debts), the disparity is even more striking, White families have a net worth of $171,000, TEN TIMES that of minority families at $17,300.

That would be because Whites are repressing Minorities in this country, and things are rapidly getting worse, not better. The primary means that this is done is via housing. In fact I became aware of this when I was using a popular real estate application, and hunting for homes in Wisconsin. I will not name the application, as I don't want to be sued. Certain homes, mostly in the inner city areas of Milwaukee, Sheboygan, Green Bay, Racine, Kenosha, Oshkosh, etc. had the first picture in each series bordered in Red or Blue. There was NO EXPLANATION for this in the software or the menu help text. In fact, I only figured out what it meant by visiting those neighborhoods.

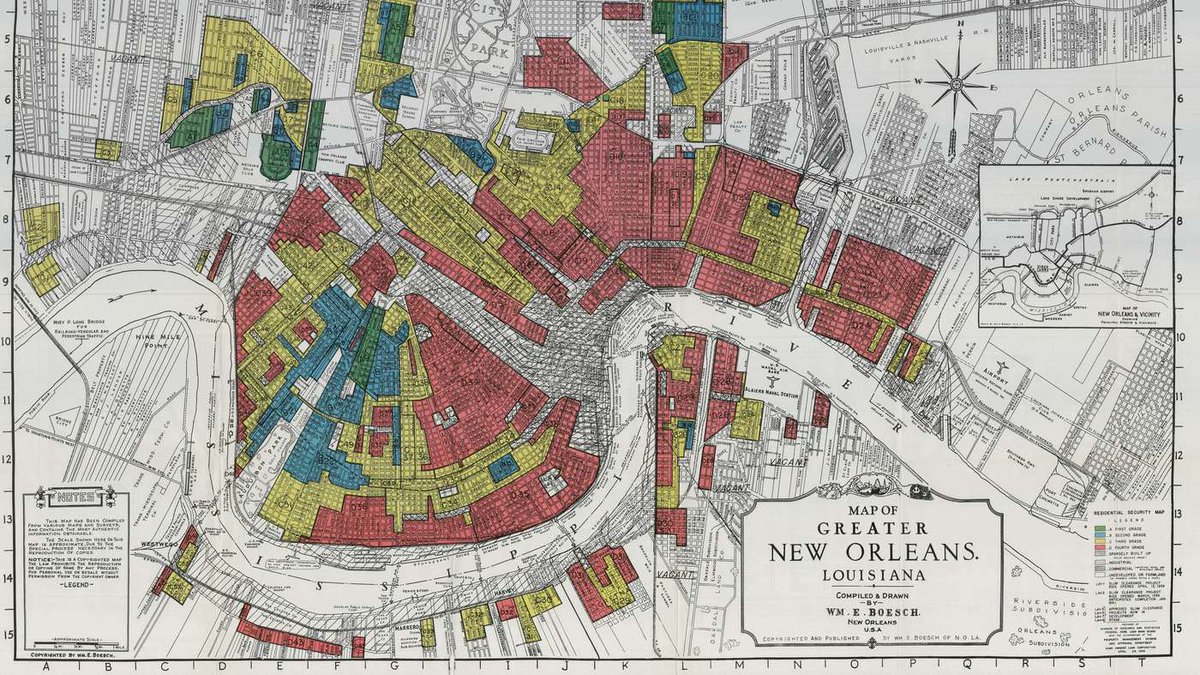

The Red borders represent "redlined" minority neighborhoods. The Blue lines represented Senior communities where people with children are being discriminated against. For those of you who don't understand the classic term "redlining", here is an older FHA map of New Orleans, LA:

Right up until 1968, for the 100 years since the Civil War, the US Federal Housing Authority discriminated against minorities, by "redlining" areas occupied by minorities where only "sub-prime" loans would be insured by the FDA, at predatory interest rates. The red areas in the above map were almost exclusively Black and Creole, and many have not yet been rebuilt from the storm damage, because - wait for it - the property owners can't get good mortgage financing,

TODAY.

My third mortgage - the initial one I got here in Silly Valley in 1986, was a sub-prime mortgage, 11.75% interest on a loan balance of more than $120,000. It hurt a lot, every month, on my relatively small paycheck. After three years, when the bank understood that I could compete in the Valley and even get promoted, I got a much better loan. I would re-finance twice more, each time lowering the interest by at least two points, before my final 15 year loan, which I paid off.

POTUS Johnson officially ended FHA racial discrimination in 1968, via the Fair Housing Act. However, racial discrimination in the USA for mortgage financing is alive and well, and as I have explained, the practice is even enshrined in the real estate applications of today.

For 262 years, the bodies of Black slaves represented wealth. In fact in 1862, the value of Black slaves in the USA was about $3 Billion, which exceeded by a considerable margin the value of the fledgling stock markets in NYC and Chicago. In fact the Civil War was fought over this wealth, and what do you suppose the Confederacy put on it's currency:

For 262 years, Black slaves built America, and the White people kept the wealth generated by them. Then in 1867 when the war was over, 101 years of official US Government discrimination in mortgage lending began. Since 1968, another 50 years of racial discrimination, this time imposed by mortgage lenders, has happened. Today, popular real estate apps clue you in the "good neighborhoods" with stable property values.

Now you understand Michelle Obama's famous remark: "Every day I wake up in a house built by Black slaves."

Now look around the neighborhood you live in. Would you move if a Black Family moved in? Or are you completely confident they won't, because you know the local mortgage lenders are protecting your property values?

Perhaps you have done your own share of oppression. This struck me when I started to consider the differences between the spectrum of skin colors in my present Silicon Valley neighborhood, and the "redlined" areas of Nantucket Island and the state of Wisconsin.